Adopting a provocative stance, the chief US economist of Goldman Sachs estimates that the rumors about the “death” of consumption, which drives 70% of the American economy, due to the flattening of incomes of poorer households have been excessively inflated.

Over the past year, especially as households were seeking relief due to problems arising from the ever increasing cost of living, many economists had assumed that a “K” shape was emerging, that is accumulation of wealth in higher income groups and flattening of the middle class, in economic data, high income households continued to prosper, while lower incomes moved away from middle class status, with their financial situation deteriorating gradually.

David Mericle of Goldman Sachs argues that this reading may have been overstated.

However, towards the end of 2026, he believes that the phenomenon will be more clearly visible, with dramatic social consequences.

At the same time, markets are making records with … steroids.

Why is this happening?

Why not stop money printing, the devaluation of the US dollar and allow stocks to trade based on fundamentals?

Because a rising stock market has now become a matter of national security.

About 58% of American households have exposure to the stock market.

In terms of real wealth, 45% of household wealth is invested in stocks.

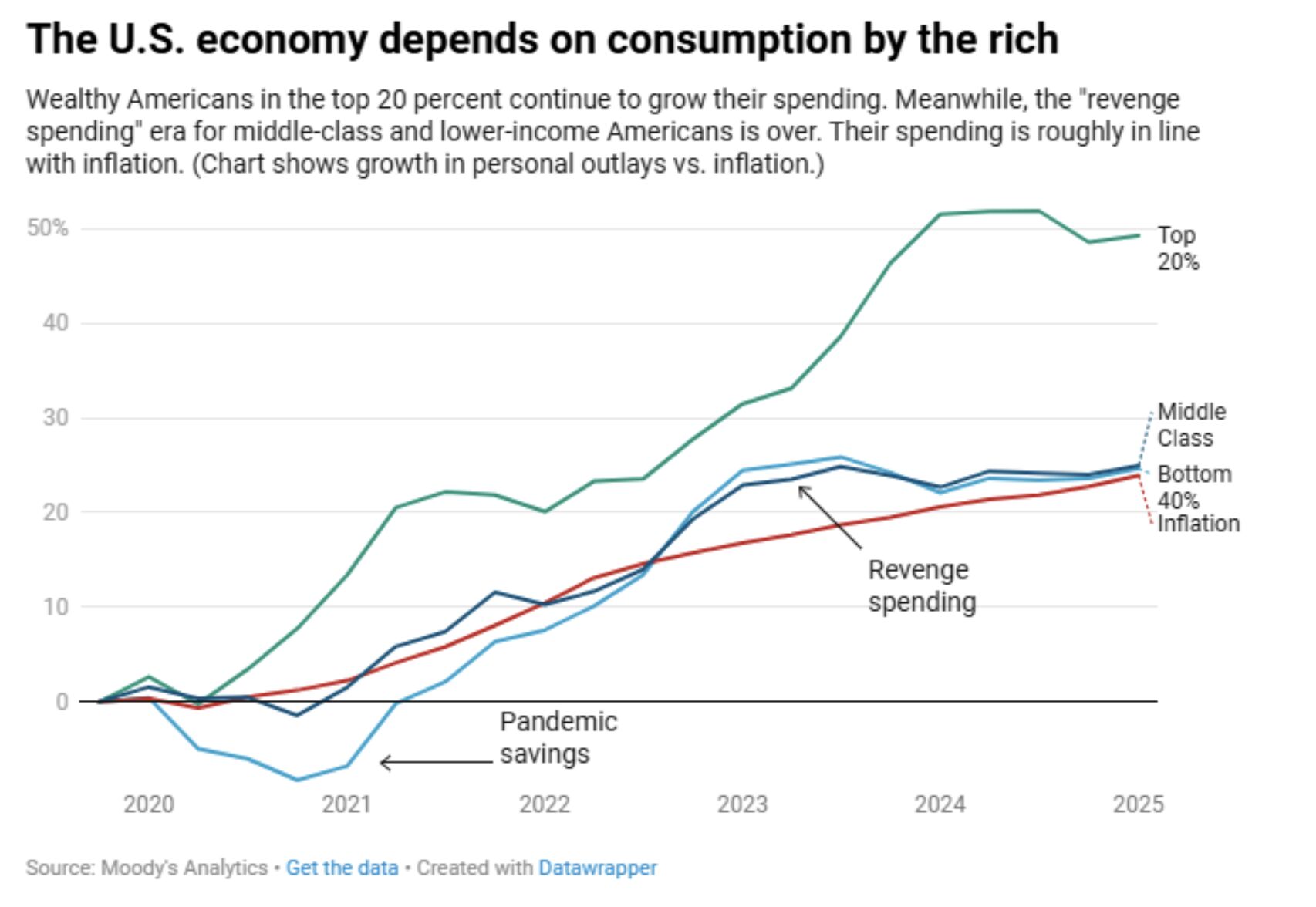

That is, almost half of the wealth held by Americans is linked to the stock market while at the same time the richest 10% of households are responsible for 58% of consumption.

Only in this context, a major downturn or crisis in stocks becomes a matter of national security in terms of economic consequences.

It is the equivalent of an economic nuclear weapon.

The S&P 500 index and the NASDAQ have both reached new all time highs.

Many commentators argue that the rise in stocks is “fake” or “manipulated”.

They are not wrong.

But they miss the main point, policymakers must manipulate stocks in order to maintain the financial system.

This does not mean that one agrees with it, the facts are simply being recorded.

The “dirty little secret” of our current financial system is that central banks cannot create jobs, increase incomes or even create economic growth.

The only thing they can do is control the price of debt or credit, something that inflates asset prices, stocks and real estate, making people feel wealthier, so that they continue to spend money.

That is all.

Who inflation bites

In December, the Goldman team wrote that “the price inflation faced by consumers of different income levels was quite similar over the past year” and that real income evolved in a similar way across the income spectrum, but with different consequences.

Weak consumption in stores serving low incomes, the team added, is likely largely due to changes in immigration policy and not because low incomes themselves are doing worse than average.

This comes in stark contrast to the view of Mark Zandi, chief economist of Moody’s Analytics.

About half of American states were essentially in recession over the past year, Zandi told Fortune, with low income consumers “hanging by a thread”.

Jack Manley, analyst at J.P. Morgan Asset Management, said in an exclusive interview with Fortune that he does not disagree with the view that immigration policy may contribute to a “K” shape in consumption data.

The dream of homeownership moves away

However, he stressed that the divergence between rich and poor has been increasing for a longer period of time, particularly in relation to a key element of the “American Dream”, housing.

“If you analyze inflation in the Consumer Price Index, where there is pressure and where it is easing, the data shows to me that the rich are doing extremely well, the poor not so well”, he explained.

“How do I see this? You look at the shelter component in the index, which is a direct and indirect measure of rents rather than home prices. Housing has long been a significant problem for inflation”.

“This inflationary pressure in housing comes from the fact that there is a shortage of homes.

People cannot buy homes, so they are forced to turn to the rental market.

Many can no longer afford perhaps the most classic element of the American Dream, that is homeownership. Thus they end up renting, and this is reflected in prices.”

Outlook will worsen for 2026

In what Goldman may agree with the “K” shaped economy scenario, is the outlook for 2026. Factors that helped consumers withstand price increases from tariffs and the rise in oil, such as the fiscal bill One Big Beautiful Bill Act and tax refunds, do not constitute permanent support for consumption.

“What initially seemed like a stable year for consumption has become more difficult”, wrote Ronnie Walker, Alec Phillips and Joseph Briggs in a note this week.

“Higher gasoline prices disproportionately affect households in the lower income category, which spend about four times a larger share of their income on gasoline compared to the upper, also affecting spending in non essential categories such as restaurants.”

They themselves forecast weak growth in consumption in the coming months, leading to a 1% decline in total retail sales.

“We continue to expect underperformance in the lower income group, due to weak job growth, cuts to Medicaid and SNAP, and now greater exposure to rising gasoline prices”, noted Goldman economists.

“We expect clearly stronger income growth in middle and higher income groups, which are less affected by the oil shock and benefit more from last year’s fiscal package.”

www.bankingnews.gr

Σχόλια αναγνωστών